Financial Forecast for Business Plan Examples for Baby Crib

![]()

![]()

DEC.11, 2017

Infant Apparel Business Plan Sample

Do you want to starting time baby clothes business?

Are y'all planning to start a baby clothes business organisation? Well, it is undoubtedly a profitable business considering the fact that around 4 million babies are built-in each year in the United States. Secondly, the article of clothing demand of babies is far too much equally compared to grown-ups hence the rate of render you volition get afterward investing in this business is simply astonishing.

The biggest reward in starting this business is that babe clothing is i of the basic necessities of people and information technology doesn't experience a downfall at any time of year, as compared to many other businesses. Before you move on to opening a baby cloth business, you lot will take to set a comprehensive business plan which will institute the basis of your company's future operations and decisions. It will help you lot determine the types of products yous volition be selling; who your target customers will exist and how you will classify your resources for the required equipment or inventory.

If you are wondering how to write an effective business plan then hither we are providing you the business plan for a baby clothes business startup named 'The Infant Finish'.

Executive Summary

2.one The Business

Start your Business concern Plan At present

Start My Concern Programme

The Baby Stop volition be an American organic and eco-friendly baby clothes manufacturer located in the Queens, the 2nd near populous borough of the New York Urban center. New York Urban center is itself the nearly populous American city housing more than viii.v million people. We volition be strategically located in an ideal location for a baby clothing business concern.

The business volition be owned and operated by Carl Dan who has been serving in the vesture industry for the last xv years. The business will be primarily involved in the large-calibration production of baby apparel including regular as well equally high cease baby boutique clothes.

2.ii Management

The Baby Stop will exist initially launched in 2 units, a production facility involved in the industry of baby clothes and a retail store for selling the products. The retail store will not just human action as a display for encouraging sales but it will also oversee the distribution of clothes amongst other retailers. The retail store volition be located in the central business commune of the city at 45 minutes from the product facility, located in the industrial zone.

Dan will manage and control the overall operations of both the production unit likewise every bit the retail store. His father Kraig Dan, who has been serving at diverse managing positions in retail giants like Wal-Mart, will bring together his son in as the shop manager and will likewise assistance him throughout the process.

2.3 Customers

The company aims to serve the residential and commercial zones of the New York City. Our customers will exist either the local residents near our retail centre or the people living in other areas of the metropolis. The showtime grouping volition buy our products directly from us while the other will buy through various retail stores scattered throughout the city.

ii.4 Target of the Company

The company aims to industry and market unique, modern, and loftier-class baby wearing apparel to our target customers. Dan'southward target is to get the best baby clothes manufacture within next five years of the launch.

Company Summary

3.one Company Possessor

Carl Dan, the possessor of the company, studied Textile Engineering from the Auburn University, Alabama, and business organization assistants from the Harvard University. Later his studies, he worked in several clothing companies at diverse positions for more than 15 years. For the final 7 years, he had been serving as the product manager of infant habiliment department in Dolce & Gabbana, US. Dan'south engineering science, likewise every bit management skills, are well-known among the high executives of the clothing industry.

3.ii Why the Business is being started

Dan had been serving at executive positions in clothing industries ranging from startups to multinational manufacturer. During his career, he had observed the ecology impact of the article of clothing manufacture, especially the toxin wastes generated during the product process. For many years he had been researching on his own to observe out the best possible ways of surround-friendly product. He wanted his own place to implement the innovative ideas in his heed which could not be applied while working in another company, even at executive positions. That's why Dan had been planning this unique startup for the terminal couple of years. Furthermore, he settled on this business due to its extremely high market place demand which will be discussed before long.

3.three How the Business volition be started

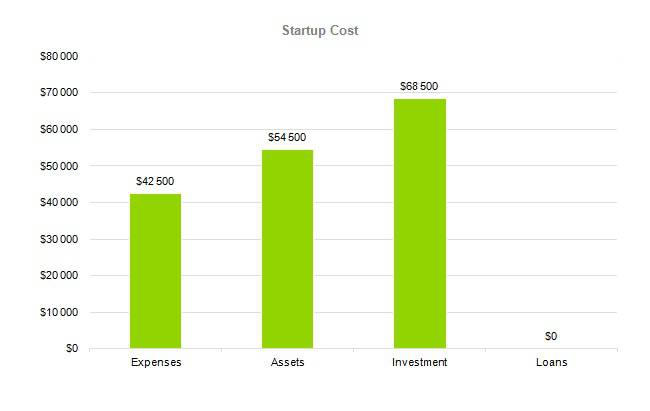

The Baby Store will be initially launched as a small business clothing shop mainly operating via a production facility and a baby boutique shop. Dan has planned everything about his business organization and has hired experts from various fields to help him arts and crafts a detailed map about information technology. The financial experts have forecasted following costs for expenses, avails, investment group for business plan, and loans for the Commencement-upwardly.

The detailed start-up requirements, start-up funding, start-up expenses, total avails, total funding required, full liabilities, total planned investment, total capital and liabilities as forecasted past experts, is given below:

| Start-up Expenses | |

| Legal | $75,500 |

| Consultants | $0 |

| Insurance | $62,750 |

| Rent | $22,500 |

| Inquiry and Evolution | $42,750 |

| Expensed Equipment | $42,750 |

| Signs | $1,250 |

| TOTAL START-Upwardly EXPENSES | $247,500 |

| Starting time-up Assets | $0 |

| Greenbacks Required | $322,500 |

| First-up Inventory | $52,625 |

| Other Current Assets | $222,500 |

| Long-term Assets | $125,000 |

| TOTAL Avails | $121,875 |

| Full Requirements | $245,000 |

| Commencement-Upward FUNDING | $0 |

| START-Upwardly FUNDING | $273,125 |

| Beginning-upwardly Expenses to Fund | $121,875 |

| First-upwards Assets to Fund | $195,000 |

| Full FUNDING REQUIRED | $0 |

| Assets | $203,125 |

| Not-cash Assets from Start-up | $118,750 |

| Cash Requirements from Offset-up | $0 |

| Additional Cash Raised | $118,750 |

| Cash Residue on Starting Date | $121,875 |

| Total Avails | $0 |

| Liabilities and Uppercase | $0 |

| Liabilities | $0 |

| Current Borrowing | $0 |

| Long-term Liabilities | $0 |

| Accounts Payable (Outstanding Bills) | $0 |

| Other Current Liabilities (interest-costless) | $0 |

| TOTAL LIABILITIES | $0 |

| Capital | $0 |

| Planned Investment | $0 |

| Investor 1 | $312,500 |

| Investor 2 | $0 |

| Other | $0 |

| TOTAL PLANNED INVESTMENT | $695,000 |

| Loss at Start-up (Commencement-up Expenses) | $313,125 |

| TOTAL Capital letter | $221,875 |

| TOTAL Majuscule AND LIABILITIES | $221,875 |

| Total Funding | $265,000 |

Services for customers

The Baby Finish volition produce following types of baby habiliment for our customers

- Leggings and pull on pants

- One-piece outfits

- Pajamas and sleepers

- Jackets and sweaters

- Shirts and pants

- Wearable blankets

We will likewise sell other baby products in our store forth with the baby clothes sale. These products will non be manufactured by us yet their presence will encourage the sales of our products. Some of those products include

- Fleece-wears and snow-suits for babies

- Shoes, socks, booties, and hats for babies

- Infant numberless, cradles, walkers, and feeders

Marketing Analysis of babe dress business

The most important component of an effective business concern plan is its accurate marketing analysis that's why Dan acquired the services of marketing experts to help him draft a proficient infant boutique business programme. After identifying the local market trends in the New York City, the marketing experts and analysts besides helped him to select the all-time site for opening the baby bazaar store.

The success or failure of a startup totally depends upon its marketing strategy for business which tin just exist developed on the basis of accurate marketing analysis. At that place are four main steps to comport out an accurate marketing analysis which are to identify the current market trends of your business concern, identify your target audience and potential customers, ready out the business concern targets to achieve, and finally set the prices of your products or services in accordance with the first 3 steps.

5.1 Market Trends

The clothing industry is one of the few industries which has seen a tremendous increase in revenue with time. The U.S. clothing marketplace is the largest in the world and was valued at a staggering amount of $359 billion in 2015. The clothing manufacturing manufacture employed effectually 90,000 people in the United States in 2015. The most interesting aspect of this manufacture is its dynamic nature. This industry is e'er changing, trying to adapt itself to the latest customer trends and new engineering that will let their shopping feel to be more ergonomic and enjoyable.

The clothing market is subdivided according to the various historic period groups of its consumers, with the most dominant beingness baby clothing. The main reason behind the increased need for baby article of clothing manufacture is that babies demand a lot of clothes, contrary to grown-ups since their clothes frequently get dirty and need to be changed time to fourth dimension. Moreover, the population is always on rising thus creating an ever-increasing demand for baby clothing products. For instance, the nascence rate in the New York City was 13.6% equally of 2015. These stats show a baby article of clothing store business can be immensely profitable provided that you market it successfully.

five.ii Marketing Division

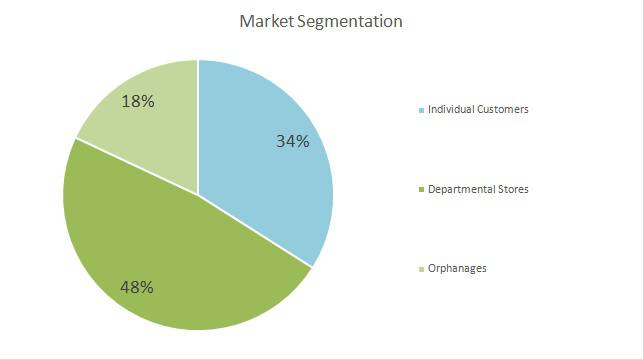

For developing a good boutique business programme it was crucial to clarify the market segmentation of the future consumers of our infant products. A successful and efficient marketing strategy can only be developed after we completely know our potential customers. Our experts have identified the following type of target audience which can become the future consumers of our babe wearing apparel:

The detailed marketing segmentation of our target audience is every bit follows:

5.ii.1 Individual Customers

One of the biggest consumers of our products will exist the community living in the residential zone of the New York City, especially the residents of the Queens borough. These private customers will buy our products directly from our store which is located in the main commercial market place of the neighborhood. These customers are pretty well-off and will thus contribute a substantial portion of our sales hence they accept a major part in deciding our strategies and policies. We will too develop various sales packages to attract these customers.

5.two.ii Departmental Stores

The Baby End will too supply its products to various departmental stores and mega malls located throughout the New York City. There are thousands of retail malls and departmental stores in the New York Urban center and most of them also sell baby clothes of diverse brands. These departmental stores will display our products forth with the products of our competitors and volition exist our second-biggest consumer afterwards the individual customers.

five.2.3 Orphanages

We volition also target the hundreds of orphanages located in Queens. These orphanages house thousands of babies each year and are constantly in demand of their clothes and other necessities. To encourage a bulk sale, we will offering discounts on various packages and volition as well provide them transportation facility to evangelize clothes to them.

The detailed market analysis of our potential customers is given in the following table:

| Market Analysis | |||||||||

| Potential Customers | Growth | Yr 1 | YEAR two | YEAR three | YEAR iv | YEAR 5 | CAGR | ||

| Individual Customers | 34% | 11,433 | 13,344 | 16,553 | 18,745 | 20,545 | xiii.43% | ||

| Departmental Stores | 48% | 22,334 | 32,344 | 43,665 | 52,544 | 66,432 | 10.00% | ||

| Orphanages | xviii% | eight,322 | nine,455 | ten,655 | 12,867 | 14,433 | fifteen.32% | ||

| Total | 100% | 42,089 | 55,143 | seventy,873 | 84,156 | 101,410 | 9.54% | ||

five.3 Business Target

Nosotros aim to go the best baby cloth manufacturing visitor of the New York City within next five years of our startup. Our master business organization targets to be achieved as milestones over the course of next three years are to achieve the net profit margin of $25k per month past the end of the kickoff yr and to rest the initial toll of the startup with earned profits by the finish of 3 years.

5.4 Production Pricing

On average our products will exist 10-xv% cheaper than our competitors. The reason behind our pricing policy is to achieve the minimum attractive rate of return while alluring maximum customers towards u.s.a..

Strategy

Dan carried out an all-encompassing enquiry before developing an effective sales strategy for the visitor. Being experienced in this industry he knew how to start a baby wearable business yet he took help from the experts so as to make this venture successful.

The sales strategy adult by our experts is as follows:

half dozen.ane Competitive Analysis:

Clothing and dress is i of the biggest industries of the United States and nearly all major wearable giants are US-based that's why nosotros have a really tough competition alee of usa.

Merely we will not come unprepared. Dan has made all preparations to shake the clothing industry from its very basis by his surroundings-friendly methods of production, releasing zero pollutants. Dan'southward idea has gained widespread attention and appreciation non simply from the United States but too around the earth. Our 2d biggest competitive edge is that our products will be 100% organic, high-quality and will price lesser than our competitors'.

6.2 Sales Strategy

Our experts take come up with the following vivid ideas to annunciate and sell ourselves.

• We volition carry out a large-scale social media campaign for our advertisement.

• We will allow our customers to buy our products online through our Facebook page. Customers can also pay online.

• We will conduct out seminars to emphasize the importance of environment-friendly production methods that will encourage customers to buy our products for the groovy crusade of reducing pollution.

• We volition initially offering discounts and gifts on our products present in several retail stores to encourage sales.

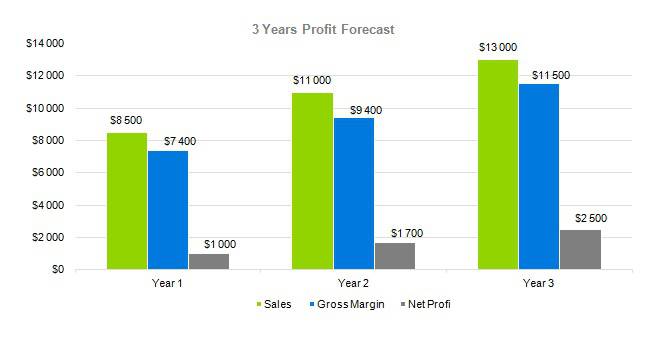

6.3 Sales Forecast

Considering our innovative idea and the quality of our products, our sales pattern is expected to increase with years. By analyzing our market segmentation strategy, our experts accept forecasted the following sales on a yearly ground which are summarized in the cavalcade charts.

The detailed information well-nigh sales forecast, total unit sales, total sales is given in the following table:

| Sales Forecast | |||

| Unit Sales | Year i | Year two | Year 3 |

| Leggings and pull on pants | 187,330 | 260,320 | 258,240 |

| One-piece outfits | 802,370 | 815,430 | 823,540 |

| Pajamas and sleepers | 539,320 | 770230 | one,002,310 |

| Jackets and sweaters | 265,450 | 322,390 | 393,320 |

| Shirts and pants | i,435,320 | one,250,430 | 1,762,450 |

| Habiliment blankets | 134,240 | 394,340 | 842,230 |

| Full Unit SALES | 3,364,030 | three,813,140 | 5,082,090 |

| Unit Prices | Year 1 | Twelvemonth 2 | Year 3 |

| Leggings and pull on pants | $140.00 | $150.00 | $160.00 |

| Jumpsuit outfits | $600.00 | $800.00 | $1,000.00 |

| Pajamas and sleepers | $700.00 | $800.00 | $900.00 |

| Jackets and sweaters | $650.00 | $750.00 | $850.00 |

| Shirts and pants | $140.00 | $120.00 | $100.00 |

| Vesture blankets | $1,150.00 | $1,300.00 | $1,450.00 |

| Sales | |||

| Leggings and pull on pants | $214,800 | $274,000 | $333,200 |

| Jumpsuit outfits | $120,050 | $194,500 | $268,500 |

| Pajamas and sleepers | $fifty,110 | $71,600 | $93,000 |

| Jackets and sweaters | $139,350 | $194,600 | $249,850 |

| Shirts and pants | $62,350 | $72,300 | $82,250 |

| Wearable blankets | $229,500 | $365,500 | $501,500 |

| Total SALES | |||

| Direct Unit of measurement Costs | Year i | Year 2 | Year iii |

| Leggings and pull on pants | $0.70 | $0.lxxx | $0.90 |

| Jumpsuit outfits | $0.40 | $0.45 | $0.50 |

| Pajamas and sleepers | $0.30 | $0.35 | $0.40 |

| Jackets and sweaters | $3.00 | $3.l | $iv.00 |

| Shirts and pants | $0.lxx | $0.75 | $0.80 |

| Wearable blankets | $three.00 | $3.50 | $4.00 |

| Direct Cost of Sales | |||

| Leggings and pull on pants | $98,300 | $183,000 | $267,700 |

| One-slice outfits | $66,600 | $119,900 | $173,200 |

| Pajamas and sleepers | $17,900 | $35,000 | $52,100 |

| Jackets and sweaters | $19,400 | $67,600 | $115,800 |

| Shirts and pants | $27,700 | $69,200 | $110,700 |

| Wearable blankets | $64,200 | $224,700 | $385,200 |

| Subtotal Directly Price of Sales | $294,100 | $699,400 | $ane,104,700 |

Personnel plan

Normally, a startup faces many problems in its initial stages. In fact, the problem is not how to start a clothing boutique or some other concern, the bodily trouble is to find the best team for your company. Dan has developed following personnel plan for his visitor.

7.1 Visitor Staff

Dan will human action as the Principal Operating Officer of the company. The visitor will initially hire following people:

- 1 Full general Manager to manage the operations of the production unit.

- 2 Administrators / Accountants to maintain financial records.

- 2 Engineers responsible for operating and maintaining production unit.

- 4 Sales and Marketing Executives responsible for delivering products to retailers and find new ventures.

- 30 Field Employees for operating the production unit and retail shop.

- four Drivers to transport products

- 1 Front Desk-bound Officer to human activity as a receptionist

To ensure the best quality service, all employees will be selected through vigorous testing and will exist trained for a month before starting their jobs.

7.2 Average Bacon of Employees

The post-obit table shows the forecasted data nigh employees and their salaries for side by side iii years.

| Personnel Programme | |||

| Year 1 | Year two | Yr three | |

| General Manager | $85,000 | $95,000 | $105,000 |

| Accountant | $45,000 | $52,000 | $59,000 |

| Engineers | $66,000 | $73,000 | $80,000 |

| Sales and Marketing Executives | $145,000 | $152,000 | $159,000 |

| Workers for Facility | $55,000 | $65,000 | $75,000 |

| Field Employees | $410,000 | $440,000 | $480,000 |

| Drivers | $60,000 | $63,300 | $70,000 |

| Front Desk-bound Officeholder | $20,000 | $23,300 | $30,000 |

| Full Salaries | $801,000 | $868,600 | $953,000 |

Financial Programme

Dan hired experts to comprise the financial aspect in the clothing business programme. The financial plan outlines the development of the company over the side by side 3 years.

8.1 Important Assumptions

The company's financial projections are forecasted on the footing of following assumptions. These assumptions are quite conservative and are as well expected to evidence deviation but to a limited level such that the company's major financial strategy will not exist afflicted.

| General Assumptions | |||

| Year 1 | Year 2 | Year 3 | |

| Plan Calendar month | 1 | 2 | 3 |

| Current Interest Rate | 10.00% | xi.00% | 12.00% |

| Long-term Interest Rate | 10.00% | 10.00% | ten.00% |

| Revenue enhancement Rate | 26.42% | 27.76% | 28.12% |

| Other | 0 | 0 | 0 |

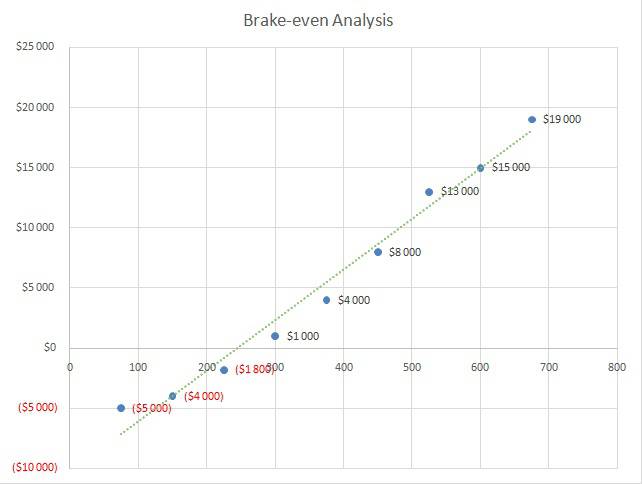

viii.2 Brake-fifty-fifty Assay

| Brake-Even Assay | |

| Monthly Units Interruption-even | 5530 |

| Monthly Revenue Break-even | $159,740 |

| Assumptions: | |

| Average Per-Unit Acquirement | $260.87 |

| Average Per-Unit of measurement Variable Price | $0.89 |

| Estimated Monthly Fixed Cost | $196,410 |

viii.three Projected Profit and Loss

| Pro Forma Greenbacks Period | |||

| Cash Received | Yr one | Year ii | Year 3 |

| Greenbacks from Operations | |||

| Cash Sales | $twoscore,124 | $45,046 | $50,068 |

| Greenbacks from Receivables | $vii,023 | $8,610 | $9,297 |

| SUBTOTAL CASH FROM OPERATIONS | $47,143 | $53,651 | $59,359 |

| Additional Cash Received | |||

| Sales Taxation, VAT, HST/GST Received | $0 | $0 | $0 |

| New Electric current Borrowing | $0 | $0 | $0 |

| New Other Liabilities (interest-free) | $0 | $0 | $0 |

| New Long-term Liabilities | $0 | $0 | $0 |

| Sales of Other Current Assets | $0 | $0 | $0 |

| Sales of Long-term Assets | $0 | $0 | $0 |

| New Investment Received | $0 | $0 | $0 |

| SUBTOTAL CASH RECEIVED | $47,143 | $53,651 | $55,359 |

| Expenditures | Year 1 | Year 2 | Yr 3 |

| Expenditures from Operations | |||

| Greenbacks Spending | $21,647 | $24,204 | $26,951 |

| Bill Payments | $13,539 | $15,385 | $170,631 |

| SUBTOTAL SPENT ON OPERATIONS | $35,296 | $39,549 | $43,582 |

| Additional Cash Spent | |||

| Sales Tax, VAT, HST/GST Paid Out | $0 | $0 | $0 |

| Master Repayment of Electric current Borrowing | $0 | $0 | $0 |

| Other Liabilities Principal Repayment | $0 | $0 | $0 |

| Long-term Liabilities Principal Repayment | $0 | $0 | $0 |

| Purchase Other Current Assets | $0 | $0 | $0 |

| Purchase Long-term Avails | $0 | $0 | $0 |

| Dividends | $0 | $0 | $0 |

| SUBTOTAL Cash SPENT | $35,296 | $35,489 | $43,882 |

| Net Cash Menses | $11,551 | $13,167 | $15,683 |

| Cash Balance | $21,823 | $22,381 | $28,239 |

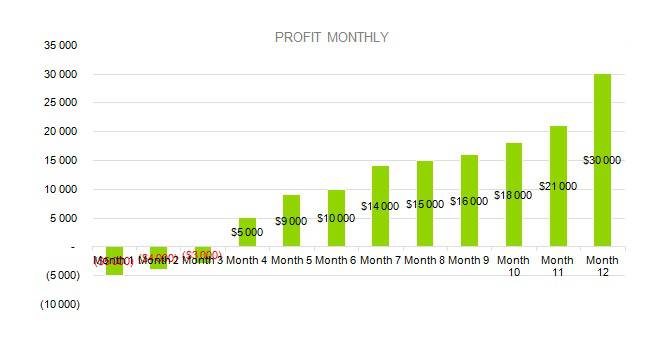

eight.3.1 Turn a profit Monthly

eight.3.ii Profit Yearly

8.3.3 Gross Margin Monthly

8.iii.4 Gross Margin Yearly

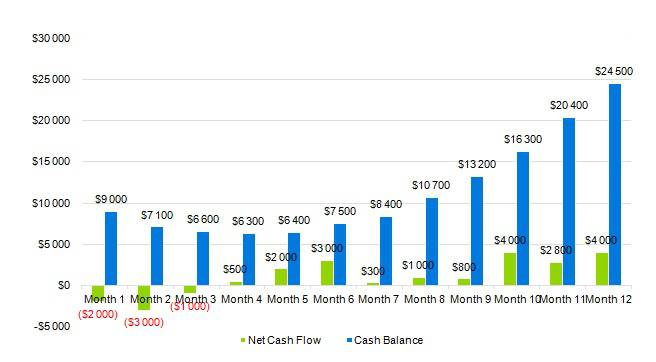

8.4 Projected Greenbacks Flow

The following table shows detailed data nigh pro forma greenbacks flow, subtotal greenbacks from operations, subtotal cash received, sub-total spent on operations, subtotal greenbacks spent.

| Pro Forma Profit And Loss | |||

| Year 1 | Yr ii | Year 3 | |

| Sales | $309,069 | $385,934 | $462,799 |

| Directly Toll of Sales | $15,100 | $xix,153 | $23,206 |

| Other | $0 | $0 | $0 |

| TOTAL Cost OF SALES | $15,100 | $19,153 | $23,206 |

| Gross Margin | $293,969 | $366,781 | $439,593 |

| Gross Margin % | 94.98% | 94.72% | 94.46% |

| Expenses | |||

| Payroll | $138,036 | $162,898 | $187,760 |

| Sales and Marketing and Other Expenses | $1,850 | $2,000 | $two,150 |

| Depreciation | $ii,070 | $2,070 | $ii,070 |

| Leased Equipment | $0 | $0 | $0 |

| Utilities | $4,000 | $4,250 | $4,500 |

| Insurance | $1,800 | $ane,800 | $one,800 |

| Hire | $6,500 | $7,000 | $7,500 |

| Payroll Taxes | $34,510 | $40,726 | $46,942 |

| Other | $0 | $0 | $0 |

| Total Operating Expenses | $188,766 | $220,744 | $252,722 |

| Profit Before Interest and Taxes | $105,205 | $146,040 | $186,875 |

| EBITDA | $107,275 | $148,110 | $188,945 |

| Interest Expense | $0 | $0 | $0 |

| Taxes Incurred | $26,838 | $37,315 | $47,792 |

| Internet Profit | $78,367 | $108,725 | $139,083 |

| Net Turn a profit/Sales | 30.00% | 39.32% | 48.64% |

eight.5 Projected Rest Sheet

The following projected residual canvas shows data nigh total electric current avails, total long-term assets, total assets, subtotal current liabilities, total liabilities, total capital, total liabilities and capital.

| Pro Forma Balance Sheet | |||

| Avails | Yr 1 | Year ii | Year 3 |

| Electric current Assets | |||

| Greenbacks | $184,666 | $218,525 | $252,384 |

| Accounts Receivable | $12,613 | $14,493 | $xvi,373 |

| Inventory | $ii,980 | $three,450 | $3,920 |

| Other Current Assets | $one,000 | $one,000 | $1,000 |

| Total CURRENT ASSETS | $201,259 | $237,468 | $273,677 |

| Long-term Assets | |||

| Long-term Avails | $10,000 | $10,000 | $x,000 |

| Accumulated Depreciation | $12,420 | $14,490 | $16,560 |

| Total LONG-TERM ASSETS | $980 | $610 | $240 |

| TOTAL ASSETS | $198,839 | $232,978 | $267,117 |

| Liabilities and Capital | Year one | Year 2 | Year 3 |

| Current Liabilities | |||

| Accounts Payable | $9,482 | $10,792 | $12,102 |

| Current Borrowing | $0 | $0 | $0 |

| Other Current Liabilities | $0 | $0 | $0 |

| SUBTOTAL CURRENT LIABILITIES | $9,482 | $10,792 | $12,102 |

| Long-term Liabilities | $0 | $0 | $0 |

| TOTAL LIABILITIES | $9,482 | $10,792 | $12,102 |

| Paid-in Capital | $30,000 | $30,000 | $30,000 |

| Retained Earnings | $48,651 | $72,636 | $96,621 |

| Earnings | $100,709 | $119,555 | $138,401 |

| Full CAPITAL | $189,360 | $222,190 | $255,020 |

| Total LIABILITIES AND Capital letter | $198,839 | $232,978 | $267,117 |

| Net Worth | $182,060 | $226,240 | $270,420 |

8.6 Business concern Ratios

The following table shows business ratios, ratio analysis, total avails, net worth.

| Ratio Analysis | ||||

| Year 1 | Year 2 | Year iii | Industry PROFILE | |

| Sales Growth | 4.35% | thirty.82% | 63.29% | 4.00% |

| Pct of Total Assets | ||||

| Accounts Receivable | 5.61% | four.71% | 3.81% | 9.70% |

| Inventory | ane.85% | ane.82% | 1.79% | 9.fourscore% |

| Other Current Assets | ane.75% | ii.02% | 2.29% | 27.40% |

| Total Current Avails | 138.53% | 150.99% | 163.45% | 54.threescore% |

| Long-term Assets | -9.47% | -21.01% | -32.55% | 58.forty% |

| Total Assets | 100.00% | 100.00% | 100.00% | 100.00% |

| Electric current Liabilities | 4.68% | iii.04% | 2.76% | 27.30% |

| Long-term Liabilities | 0.00% | 0.00% | 0.00% | 25.eighty% |

| Total Liabilities | 4.68% | 3.04% | 2.76% | 54.10% |

| Net WORTH | 99.32% | 101.04% | 102.76% | 44.90% |

| Pct of Sales | ||||

| Sales | 100.00% | 100.00% | 100.00% | 100.00% |

| Gross Margin | 94.18% | 93.85% | 93.52% | 0.00% |

| Selling, Full general & Administrative Expenses | 74.29% | 71.83% | 69.37% | 65.20% |

| Advertising Expenses | 2.06% | 1.11% | 0.28% | i.twoscore% |

| Turn a profit Before Interest and Taxes | 26.47% | 29.30% | 32.13% | two.86% |

| Master Ratios | ||||

| Current | 25.86 | 29.39 | 32.92 | one.63 |

| Quick | 25.iv | 28.88 | 32.36 | 0.84 |

| Total Debt to Total Assets | two.68% | ane.04% | 0.76% | 67.10% |

| Pre-taxation Return on Internet Worth | 66.83% | 71.26% | 75.69% | 4.40% |

| Pre-revenue enhancement Return on Avails | 64.88% | 69.75% | 74.62% | 9.00% |

| Additional Ratios | Year ane | Twelvemonth 2 | Yr 3 | |

| Net Profit Margin | nineteen.20% | 21.16% | 23.12% | Due north.A. |

| Render on Equity | 47.79% | 50.53% | 53.27% | North.A. |

| Activity Ratios | ||||

| Accounts Receivable Turnover | 4.56 | 4.56 | 4.56 | N.A. |

| Collection Days | 92 | 99 | 106 | Due north.A. |

| Inventory Turnover | 19.7 | 22.55 | 25.4 | N.A. |

| Accounts Payable Turnover | fourteen.17 | 14.67 | 15.17 | N.A. |

| Payment Days | 27 | 27 | 27 | N.A. |

| Total Asset Turnover | 1.84 | 1.55 | 1.26 | Northward.A. |

| Debt Ratios | ||||

| Debt to Net Worth | 0 | -0.02 | -0.04 | N.A. |

| Current Liab. to Liab. | 1 | ane | i | N.A. |

| Liquidity Ratios | ||||

| Internet Working Capital | $120,943 | $140,664 | $160,385 | N.A. |

| Involvement Coverage | 0 | 0 | 0 | N.A. |

| Additional Ratios | ||||

| Assets to Sales | 0.45 | 0.48 | 0.51 | N.A. |

| Current Debt/Total Assets | four% | iii% | 2% | N.A. |

| Acid Test | 23.66 | 27.01 | 30.36 | North.A. |

| Sales/Cyberspace Worth | 1.68 | 1.29 | 0.nine | Northward.A. |

| Dividend Payout | 0 | 0 | 0 | North.A. |

Download Baby Clothes Concern Plan Sample in pdf

OGScapital too specializes in writing business plans such as babe boutique business organization plan, starting a bazaar store, business plan of a bridal shop, business plan sample for habiliment line, clothing store business organisation plan, shoe concern plan and many others business plans.

See besides

Any questions? Get in Touch!

Nosotros have been

mentioned in the press:

Source: https://www.ogscapital.com/article/baby-clothes-business-plan-sample/

{kind=link}

Post a Comment for "Financial Forecast for Business Plan Examples for Baby Crib"